alexsoto22

Alejando Sotolongo

Recently Published

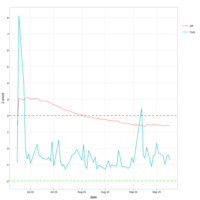

Country Equity AR and Turbulence

z-scores of turbulence and absorption ratio from equity etfs

for paperback investing post

Risk Report March 2016

Risk report proto-type.

Currently measures fragility based on Kritzman et al 2010 with US equity sectors and global assets

Plan to add more on option skewness and implicit jump parameters (from Bates 1991), also implied vol surface of S&P 500

French Fama Carhart Example

Multi-factor regression that uses the market plus size, style, and momentum factors to explain an equity security's systematic risk. Publication shows how to: 1) parse factors from French's online research library, 2) clean the data, and 3) run a multi-factor regression and analyze the results

Implied_Vol

code to parse option chain data from google finance and calculate an implied volatility smile from the option prices and strikes

Risk Parity Solution

Application of Newton's method in linear algebra form to solve for portfolio weights that force each security to contribute an equal amount of component portfolio risk (i.e., risk parity). Algorithm is presented as two functions and a for loop and then tested with a hypothetical portfolio of sector ETFs.

Volatility Risk Budget

Example of how to conduct a risk budget analysis on a portfolio. Risk in this example is standard deviation or volatility, and a hypothetical portfolio of tech stocks are used for the analysis.