rmerrima

Bobby Merriman

Recently Published

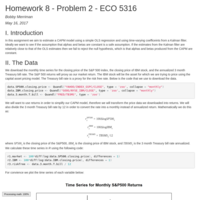

ECO 5316 - Homework 8 - Problem 2

Uses a state space model approach, specifically a Kalman filter, to estimate the alpha and beta coefficients of the CAPM model. We then compare these time-varying estimates to the estimates using an OLS framework.

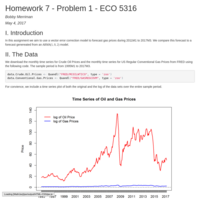

ECO 5316 - Homework 7 - Problem 1

Employs a VEC model to forecast future gas prices from past gas and oil prices. Compares the VEC forecast to that of an ARMA model. The VEC forecast far outperforms the ARMA model. Also shows tests of co-integration.

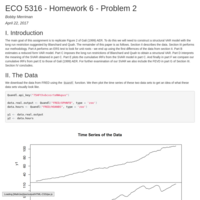

ECO 5316 - Homework 6 - Problem 2

Replicates Figure 2 of Gali (1999) AER. Uses a VAR and an SVAR model. Looks at cumulative impulse response functions (IRFs) and forecast error decomposition variances (FEVDs) of the SVAR model.

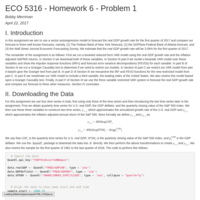

ECO 5316 - Homework 6 - Problem 1

Uses a two and three variable VAR model. Tests for Granger Causality. Examines impulse response functions (IRF) and forecast error variance decomposition (FEVD). Specifically, uses a three variable VAR model to forecast next quarter's real GDP growth rate.

ECO 5316 - Homework 5 - Problem 2

Uses Intervention Analysis to analyze Retail and Food Service Sales data. The intervention in this analysis is the impact of the 2008 recession. Also incorporates seasonality and Box-Jenkins methodology. We find that an ARIMA(11,1,0)(2,0,0) model best forecasts monthly RFSS data.

ECO 5316 - Homework 5 - Problem 1

Uses Box-Jenkins methodology to determine the best forecasting model of Total Private Residential Construction Spending data. Specifically, we control for seasonality, differencing, and use a log transformation of the data. Uses a multi-step and rolling scheme forecast.

ECO 5316 - Homework 4

Uses the ADF, KPSS, and ERS tests to check for trend vs. difference data. The appendix is useful as it provides a generalized code that will run the ADF, KPSS, and ERS tests on any data for any amount of differences.

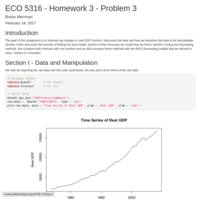

ECO 5316 - Homework 3 - Problem 3

Time series forecasting of log changes in real GDP. Splits the sample for both in and out of sample performance. Uses a multi-step and rolling scheme forecasting method. Compares the forecasting ability of the best in-sample model to the forecast ability of an AR(1) model.

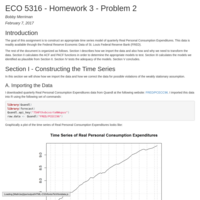

ECO 5316 - Homework 3 - Problem 2

Time series model of real personal consumption expenditures. Uses ACF and PACF functions to determine AR, MA, and ARMA models. Analysis of models is given as well.