valueedge

Leonardo Zepeda

Recently Published

Recent Financial Cycles

By analyzing DOW and S&P indexes from 1980 to date, the author identifies 7 financial cycles and present common statistical features and parameters for each cycle. The analysis found that a cycle’s length range from 714 to 1,777 days, averaging 20 basis points (bp) and 101 bp weekly and monthly returns respectively for DOW index; and 17 bp and 96 bp weekly and monthly returns respectively for S&P index. The analysis also found that cycle’s total returns averaged 1.56 and 1.60 times it initial values for DOW and S&P indexes respectively, ranging from 1.38 to 1.81 times for both indexes.

With the latest, and considering only statistical features, we could infer current cycle still have 251 days left with the expectation to deliver at least 1.58 times its initial values, from which DOW has ran 92% of it already, and S&P has surpassed 2% above its peak already. The analysis also infers that negative returns will be the norm on a weekly and monthly basis and by now, this cycle still have around 20 -50 negative records to go to reach cycles’ average. Also that there is not a noticeable trend for immediate recovery after sensitive falls. However, at the end of the cycle, positive shots should compensate incidental losses by the end of the cycle.

Punta San Francisquito

Descriptive facts of Punta San Francisquito

Rental Business Opportunities 4 Cities

With official information from the Federal Reserve of the United States and Zillow.com, from January 2019 to December 2021, we analyze the behavior of inventory, prices and rental value of housing in the cities of Miami, Dallas, Houston, Austin, Denver, Phoenix, Los Angeles and San Diego.

The following pages will illustrate how:

For Cash Flow Generation Opportunities through the purchase-sale of units. Considering the volume and dynamics of the market, it is concluded that given the recent inventory contractions, there is a considerable appreciation opportunity for real estate in all 4 Metros. Miami’s sustained decrease in inventory and comparatively lagged price increases, suggest Miami as the most attractive destination.

For Cash Flow Generation Opportunities through the exploitation (rental) of units Of the analyzed Metros, Denver and Dallas present the highest rental recovery values (5.25 and 5.21% per year respectively). However, Miami and Houston seem to have the best dynamics of potential rent catching-up adjustments with respect to prices, therefore with higher potential for profit.

Residential Real Estate Opportunities in the US

With official information from the Federal Reserve of the United States and Zillow.com, from January 2019 to January 2022, we analyze the behavior of inventory, prices and rental value of housing in the cities of Miami, Dallas, Houston, Austin, Denver, Phoenix, Los Angeles and San Diego.

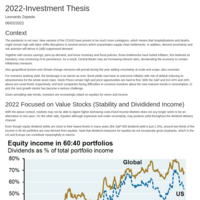

2022-Investment Thesis

Health issues have exacerbated supply-chain bottlenecks. In addition, derived uncertainty and risk aversion might still derive in suppressed demand. Together with excess savings, pent-up demand, and loose monetary and fiscal policies, the context have fueled persistant inflation. As a result, Central Banks may act increasing interest rates, decelerating the economy to contain inflationary menaces.

For investors seeking yield, the landscape is as barren as ever. Fixed Income might not be paying its increasing risk premium and Stock Prices remain expensive with price opportunities hard to find. Also, tech companies face increasing difficulties to convince investors about the next massive trends in consumption, so, to pick the next growth stocks has become a serious challenge.

With that Context, , we believe the only opportunities for yield rely on Value Stocks either looking for dividend yield or by active trading strategies.

This document present an assestment, construction and backtesting for 3 portfolios formed with the top 15 highest-dividend-yield Value Stocks.